How Do I Know If My Bookkeeping Is Wrong?

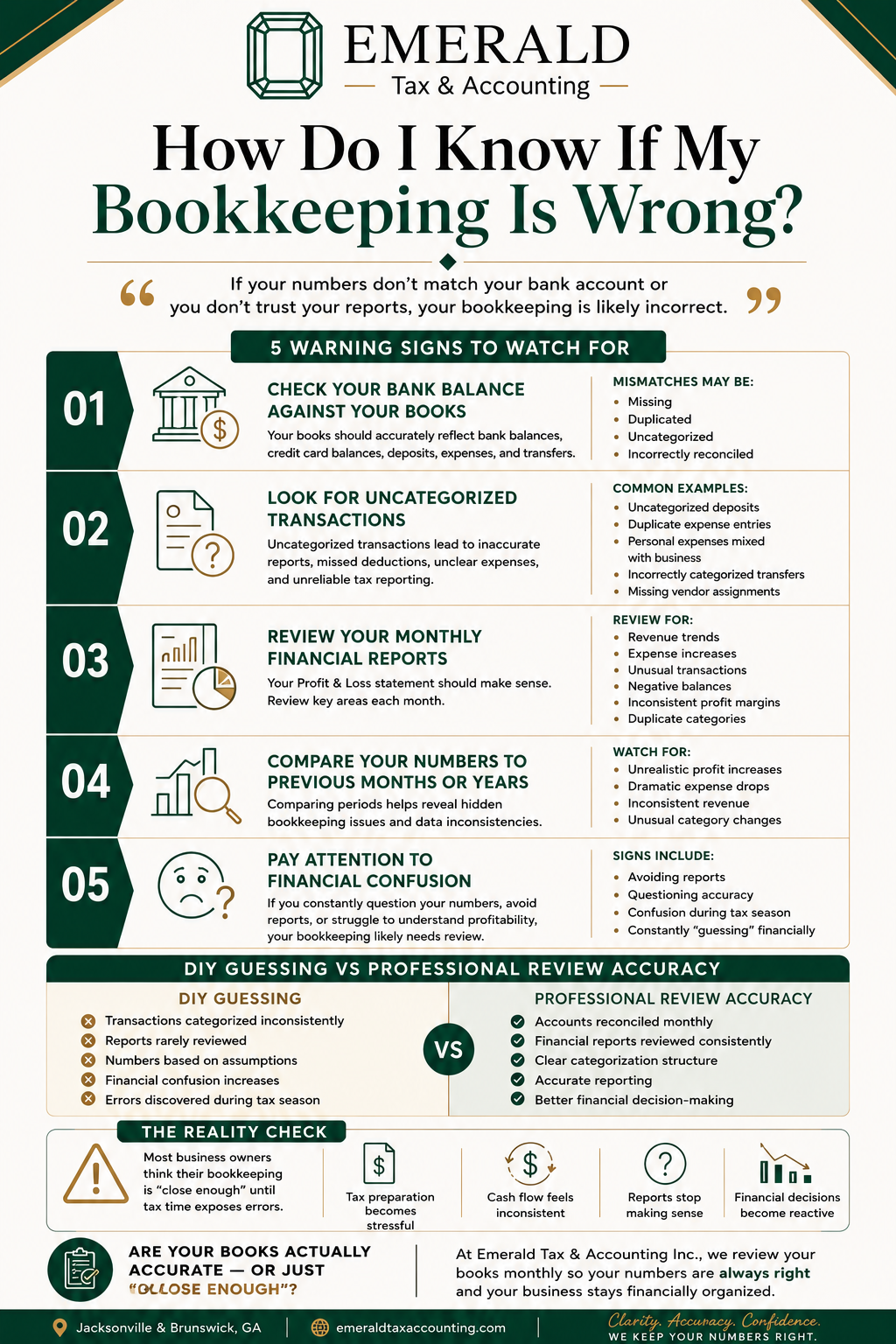

If your bookkeeping numbers do not match your bank account, your reports feel inaccurate, or you constantly question your financial information, your bookkeeping is likely incorrect.

Many business owners assume their bookkeeping is “mostly fine” until:

reports stop making sense

tax season becomes stressful

cash flow feels inconsistent

accounts no longer reconcile

Small bookkeeping problems create larger financial confusion over time.

Accurate bookkeeping is the foundation of financial clarity.

Here are some of the biggest warning signs your bookkeeping may need attention:

The How-To Steps

1. Compare Your Bank Balance to Your Books

One of the biggest warning signs of bookkeeping problems is when your reports do not match your actual bank account balances.

Your bookkeeping should accurately reflect:

bank balances

credit card balances

deposits

expenses

transfers

If your reports show different numbers than your accounts, something may be:

missing

duplicated

uncategorized

incorrectly reconciled

Small bookkeeping discrepancies often turn into larger financial problems over time.

2. Look for Uncategorized Transactions

Uncategorized transactions are a major sign that bookkeeping is incomplete.

When transactions are not categorized correctly:

reports become inaccurate

deductions may be missed

expenses become unclear

tax reporting becomes unreliable

Common examples include:

uncategorized deposits

duplicate expense entries

personal expenses mixed with business

incorrectly categorized transfers

The longer bookkeeping stays disorganized, the harder financial clarity becomes.

3. Review Your Monthly Financial Reports

Many business owners generate financial reports without actually reviewing them.

Your reports should make sense.

If your Profit & Loss statement feels confusing or inaccurate, that is usually a sign that bookkeeping needs attention.

Review:

revenue trends

expense increases

unusual transactions

negative balances

duplicate categories

Bookkeeping should create clarity — not confusion.

4. Compare Your Numbers to Previous Months or Years

Comparing your current numbers to previous reporting periods can reveal hidden bookkeeping errors.

Watch for:

unrealistic profit increases

dramatic expense drops

inconsistent revenue

unusual category changes

Sometimes the issue is not business performance.

Sometimes the issue is inaccurate bookkeeping data.

5. Pay Attention to Financial Confusion

One of the most overlooked warning signs is constantly feeling unsure about your numbers.

If you:

avoid looking at reports

question whether numbers are accurate

feel confused during tax season

struggle to understand profitability

constantly “guess” financially

your bookkeeping likely needs review.

Accurate bookkeeping should help business owners feel informed and confident — not stressed and uncertain.

DIY Guessing vs Professional Review Accuracy

DIY Guessing

Transactions categorized inconsistently

Reports rarely reviewed

Numbers based on assumptions

Financial confusion increases

Errors discovered during tax season

Professional Review Accuracy

Accounts reconciled monthly

Financial reports reviewed consistently

Clear categorization structure

Accurate reporting

Better financial decision-making

The Reality Check

Most business owners think their bookkeeping is:

“close enough.”

Until:

tax preparation becomes stressful

deductions are missing

cash flow feels inconsistent

reports stop making sense

financial decisions become reactive

Bookkeeping problems usually build slowly before they become obvious.

That is why consistent monthly review matters.

Are your books actually accurate — or just “close enough”?

Good bookkeeping creates:

clarity

confidence

better decisions

cleaner tax preparation

healthier business operations

Your financial reports should help you lead your business with confidence — not uncertainty.

At Emerald Tax & Accounting Inc., we review bookkeeping monthly so business owners always understand their numbers and stay financially organized year-round.